Uncertainty is rewriting the rules of startups in MENA

- April 30, 2026

- 0

The current slowdown in the MENA startup ecosystem is no longer just a temporary dip in funding flows—it appears to be a deeper shift that is reshaping how

The current slowdown in the MENA startup ecosystem is no longer just a temporary dip in funding flows—it appears to be a deeper shift that is reshaping how

The current slowdown in the MENA startup ecosystem is no longer just a temporary dip in funding flows—it appears to be a deeper shift that is reshaping how the entire system operates.

After a strong start to 2026, investment activity slowed noticeably amid rising geopolitical tensions in the region, prompting investors to adopt a more cautious stance and reassess risk.

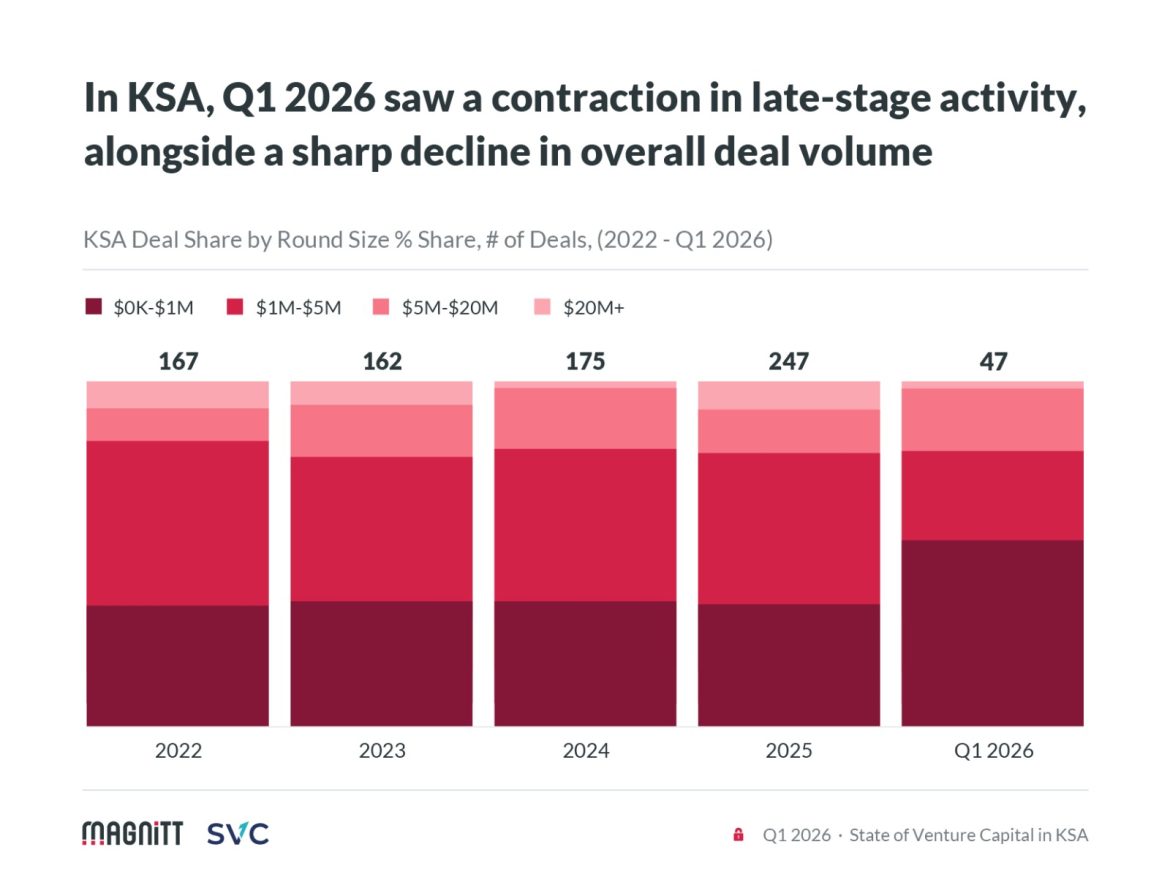

In Q1, investments fell to around $941 million, down more than 20% compared to the previous quarter.

March was particularly telling, marking one of the weakest months in recent years.

However, this was not a collapse in capital, but rather a slowdown in deal execution—capital did not disappear, it simply entered a “waiting mode.”

It reflects not just valuations or sector performance, but a broader change in market dynamics: investment decisions are taking longer, timelines are stretching, and funding deployment is becoming more selective and cautious.

closely tied to expanding funding sources and strong investor appetite for rapid scaling. That model is now under clear pressure.

Investors—including state-backed sovereign wealth funds—are revisiting their strategies amid a more volatile global and regional environment.

According to estimates from Global SWF, sovereign wealth funds in the Middle East have played an increasingly important role in global tech and infrastructure deals.

However, their investment pace tends to slow during periods of instability, reinforcing a broader sense of caution across the ecosystem.

This shift is clearly reflected in startup behavior.

Growth is still the goal, but it is now being managed with greater discipline. Founders are reassessing expansion plans, tightening cost structures, and prioritizing financial sustainability.

This is less a change in ambition and more a direct response to a funding environment that is less predictable and more volatile.

In this environment, financial management is no longer a secondary function—it sits at the core of every decision.

Startups are now planning for much longer runways than before. Where 18 months once provided a sense of security, many companies are now planning for up to 30 months of operations.

Spending behavior has also shifted. Instead of broad cost-cutting, companies are making more precise decisions: identifying where spending generates clear returns and where it can be delayed.

Non-core initiatives are being postponed, while activities directly tied to revenue generation are being protected.

At the same time, fixed costs are being reassessed, contracts renegotiated, and long-term commitments reduced wherever possible.

There is also a stronger focus on financial monitoring. Instead of periodic reviews, many startups now track performance on a weekly basis, enabling faster responses to changes in revenue or expenses.

This reflects a clearer understanding that resilience depends not just on the amount of capital available, but on how efficiently it is managed.

Sequoia Capital, for example, has consistently advised founders during downturns to operate under the assumption that external funding may not be readily available—an assumption that now feels increasingly relevant in the region.

Cost pressures often lead to layoffs, but job cuts are not the only response.

Many startups in the region are first changing how teams operate in order to preserve talent while improving efficiency.

Teams are becoming smaller in size but broader in responsibility.

Roles are being merged, and employees are expected to take on multiple functions.

This reduces the need for constant hiring while increasing internal flexibility.

At the same time, more activities are being shifted to flexible cost models, including external partners or usage-based arrangements.

Hiring plans are also being reconsidered. Instead of aggressive expansion, non-essential roles are being delayed, with a stronger focus on retaining core talent.

The logic is simple: when conditions improve, execution speed will depend heavily on the strength and continuity of the existing team.

As demand patterns evolve, it is no longer just about how much revenue a company generates, but the nature of that revenue.

Startups relying on discretionary spending or long, complex enterprise deals are more exposed to sudden shifts in customer behavior.

In contrast, companies with recurring revenue models or essential services tend to show greater stability.

Despite the overall decline in funding, certain sectors continue to attract investor interest, including fintech infrastructure, B2B software, and logistics.

These industries share a common trait: relatively predictable cash flows and essential operational demand.

For startups, this means a stronger emphasis on not just growing revenue, but ensuring its durability under pressure—speed of collection, customer retention, and focus on stable-demand sectors are becoming central to strategy.

The region’s market diversity is often seen as a growth advantage, but it also introduces uneven risk exposure.

Economic conditions vary significantly between markets, particularly between the Gulf and more fragile economies facing inflationary pressure and currency volatility.

As a result, startups are becoming more selective in their regional expansion. GCC markets, supported by liquidity and government initiatives, are seen as more stable environments.

Meanwhile, expansion into higher-risk markets is being slowed or adjusted, including pricing revisions to reflect local volatility.

This does not signal a retreat from regional ambition, but rather a near-term reordering of priorities toward stability and predictability.

Fundraising itself has become more complex. Deals are taking longer to close, investors are more selective, and valuations are generally more conservative.

In response, founders are starting fundraising conversations earlier and investing more time in building investor relationships.

The market is gradually shifting away from fast transactions toward longer-term alignment between startups and investors.

At the same time, alternative financing options are becoming more visible, including venture debt and strategic partnerships, as companies diversify their capital sources.

This reflects a broader shift in power dynamics: capital is still available, but it is more selective and comes with higher expectations around resilience and performance.

In moments like these, the difference between fast-growing companies and durable ones becomes clear.

In a region where external shocks are increasingly part of the business environment, resilience is emerging as a core competitive advantage.

Startups are being pushed to make more deliberate choices about how they operate—how they spend, how they structure teams, and how they approach growth.

While these decisions are often difficult, they are shaping a more disciplined generation of companies.

When conditions eventually stabilize, the companies that survive this phase are unlikely to return to the same growth models.

Instead, they will operate with stronger foundations, clearer priorities, and a deeper understanding of risk.

In that sense, this period is not only a constraint—it is also a filter.

The companies that pass through it will be best positioned to define the next phase of the region’s startup ecosystem.